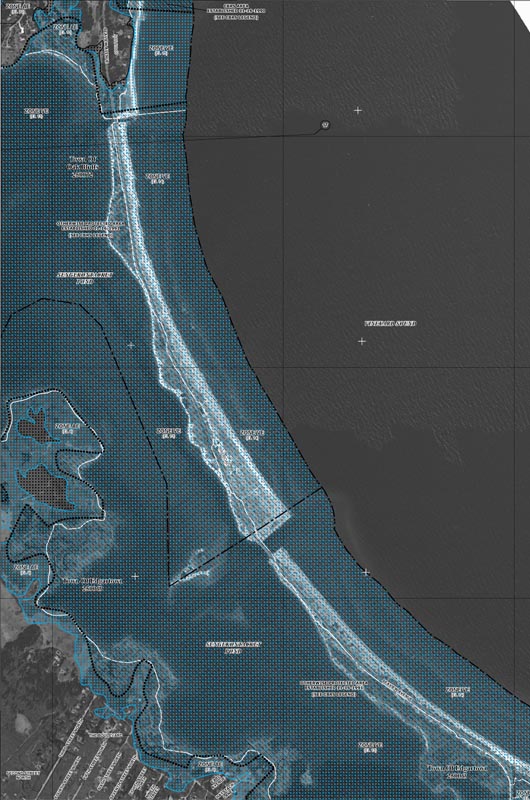

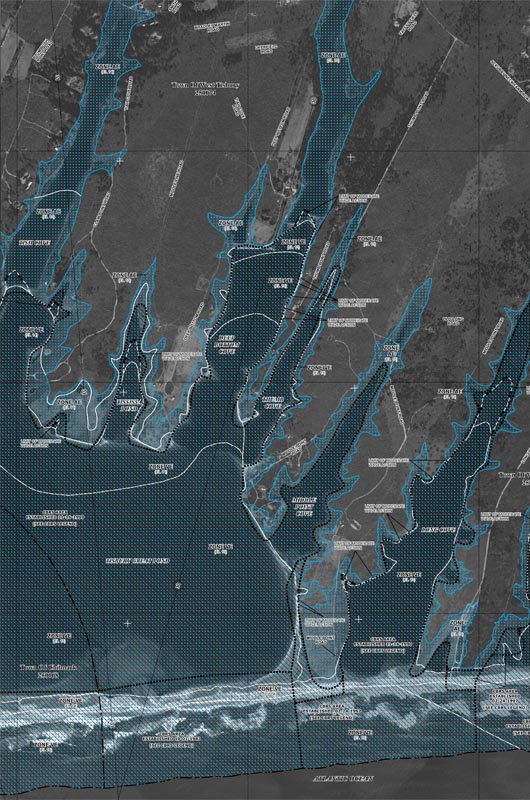

<p>The Federal Emergency Management Agency has released updated preliminary floodplain maps that predict increased flooding in coastal areas during northeasters, gales and other strong storms. The maps are the first significant update since the mapping program began in the 1980s and are expected to directly affect federal flood insurance premiums for towns and counties, as well as mortgage programs for some homeowners.</p>

The Federal Emergency Management Agency has released updated preliminary floodplain maps that predict increased flooding in coastal areas during northeasters, gales and other strong storms. The maps are the first significant update since the mapping program began in the 1980s and are expected to directly affect federal flood insurance premiums for towns and counties, as well as mortgage programs for some homeowners, once they are made final sometime late this year.

The maps are currently available for public inspection online.

Beach Road.

Beach Road.

They demarcate flood hazard areas in Dukes County, and predict increased flooding for coastal, lakeside and river areas due to all-new modeling and more stringent criteria.

The maps have been periodically updated since the 1980s, but until now have been based on the same modeling and much of the same topographic data as when they were first published.

The new maps are created using LIDAR data, which was added to the 2010 map edition and is collected from an airplane, and all-new base flood elevation modeling. The Strategic Alliance for Risk Reduction (STARR), contracted by FEMA, measured the topography across 64.2 square miles of Dukes County coastline in 2011 and developed the maps using high-tech modeling. LIDAR technology stands for Light Detection and Ranging. It is a remote sensing tool that emits and reflects laser light off a target area on land to calculate elevation.

“What they come up with is a very accurate picture of the topography,” said Jo-Ann Taylor, coastal planner at the Martha’s Vineyard Commission. She said when you compare an old map with an updated, LIDAR-produced map, the difference is remarkable. “It’s like looking like at something done with a crayon by a kindergartner side by side with something done by a precise machine . . . the boundaries of the different zones are much more precise,” she said.

Regions marked with a “VE” or “AE” present the highest risk for coastal flooding; a 26 per cent chance of flooding over the course of a 30-year mortgage. Many of the most vulnerable areas are rated higher risk in these maps than those published before, which is a result of the inclusion of more flood-risk criteria.

Tisbury Great Pond.

Tisbury Great Pond.

Though the maps are published for regulatory reasons, the designations are not final yet. The maps will not affect insurance premiums until they become final, a process which will take at least six months, said Kerry Bodgan, a senior engineer with FEMA.

At the current stage, the maps are made available so that the general public can weigh in and verify the accuracy of the data collected. For example, if a map incorrectly names a street, or marks an area dry that is known to be often flooded, people can submit corrections. Towns have had access to the maps for a few months and have been encouraged to comment as well. Planners, like Ms. Taylor, also use the data to inform their decisions about safe practices. Once FEMA finalizes the maps, towns have six months to comply with their designations, or risk suspension from the National Flood Insurance Program.

The maps are of particular interest to homeowners who live in flood hazard zones AE and VE, where they predict increased wave height and greater area vulnerable to flooding when compared with previous maps. “Even if it shows that [their] house is in a different flood category [than before], it’s not going to change their insurance rate until final rates are published,” Ms. Taylor said. But she cautions against disregarding the maps altogether. “If I were a property owner [in a flood hazard zone], I would take it very seriously as well,” she said.

Structures built within high-risk areas are eligible for national flood insurance coverage. A major exception is Chilmark, which is the only one of the six Island towns that does not participate in the National Flood Insurance Program. The floodplain bylaw would have required the houses in Menemsha to be built on stilts, Ms. Taylor said. As a result, homeowners there cannot purchase flood insurance through the federal program.

Chilmark has never participated in the flood insurance program, and it looks like they will opt out for at least another five years, said Tim Carroll, director of emergency management and the town executive’s secretary. At a meeting Tuesday night, selectmen voted to take no action regarding the flood maps. “We don’t allow people to build in the hazard zones,” Mr. Carroll explained. “Very few homes [in Chilmark] are impacted by a northeaster.”

Though flooding caused by northeasters can cause a lot of damage to property, especially in areas below sea level, storm surges, which occur during hurricanes, cause the greatest loss of life and property. Insurance companies do not consider storm surge data in their analyses of risk, nor do they factor in the effects of sea level rise. Therefore, the maps are not a “be-all and end-all tool for assessing vulnerability,” Ms. Taylor said, especially for planning purposes. Mr. Carroll estimates that 30 Chilmark homes are vulnerable to hurricane surge, but the National Flood Insurance Program does not cover these areas. Chilmark posts storm surge maps on the town website.

Leonard Jason Jr., building inspector in Edgartown and Chilmark, said insurance companies drive the mapping projects. “I think they were designed originally because the federal government got tired of paying people to rebuild their houses,” Mr. Jason said. Once the flood zones are determined by FEMA, the insurance companies “raise the rates and minimize their risk, and the government helps them,” Mr. Jason said.

The maps are “generally speaking” more conservative, as a result of the addition of wave setup and wave runup to the analysis, Ms. Bodgan said. Wave setup is the piling up of waves on a shoreline during stormy weather, and wave runup is the calculation of how a wave interacts with an uneven shoreline — if it’s rocky or features a barrier like a seawall.

The maps can be viewed at FEMA's website.

Comments

Anyone got a key to the

Christopher Gray Republic of ChappaquonsettAnyone got a key to the individual maps? Or am I missing something?

The last pdf in the long list

Steve OBThe last pdf in the long list of rate maps is the index.

I'm on Senge. This happened

Scott EdgartownI'm on Senge. This happened to me two years ago when they changed the maps. When I bought the house, I wasn't in a flood zone. The new map has me in the worst zone - VE. When I went to price out flood insurance, I was told $40k per year. That's not a typo. $40k per year. My house was built in 1946 and has never, ever been flooded. Not even close. The dirty secret of Flood Insurance is that it isn't really insurance at all - it's a government subsidy that is priced with absolutely no relationship to risk and payout. The max coverage is $250,000. At $40k per year, the premiums would pay the maximum payout every four years. There is no insurance policy in existence that is based on actuarial analysis where that premium/payout ratio exists. I'm sorry that the program has been severely stressed by recent weather disasters that wiped out huge swaths of residential and commercial buildings in areas that should have never been built up in their existing manner, but that's not my problem and I shouldn't have to pay for it. If these new rates come into play, the impact on the market value of coastal properties will be significantly affected as non-cash buyers have to factor in the exorbinant cost of flood "insurance". Make no mistake - this is a tax, not insurance.

Scott, flood insurance is not

Steve FalmouthScott, flood insurance is not a tax. A tax is something you are required to pay by law. I dont think you are required to buy flood insurance. If you think it is too expensive, then go without!

To have a mortgage in a flood

Doug MacIVER Lake AveTo have a mortgage in a flood zone you are required to have flood insurance

Most people need a mortgage

Kathryn New Canaan CTMost people need a mortgage to buy. Banks require flood insurance. Bottom line, insurance companies stopped being insurance companies in recent decades and stopped offering insurance, as they found they had to pay out. The gift took over offering flood insurance and of course, the foot mingles monies and spends at will. Case in point, most who have paid for flood insurance are still out of their homes after sandy and the time frame for coverage is coming to an end. So, too bad for those who paid for something & the govt doesn't give them what they paid for. We have to stop thinking the govt will take care of everything. Frankly, we shouldn't be building in areas where flooding is possible, or below sea level.

Scott, I live near Sengy too

Elsbeth EdgartownScott, I live near Sengy too and will fall in the flood zone in the new maps. Bad news, it just passed at the town meeting to accept the new maps. There were only two of us that voted not accept the maps.

Add new comment